John Knox Village is a prestigious Retirement Community highly regarded and sought after by seniors nationwide. Learn why seniors love life at John Knox village, how they fund their Entry Fee as they transition to this beautiful community, and download a helpful Funding Guide.

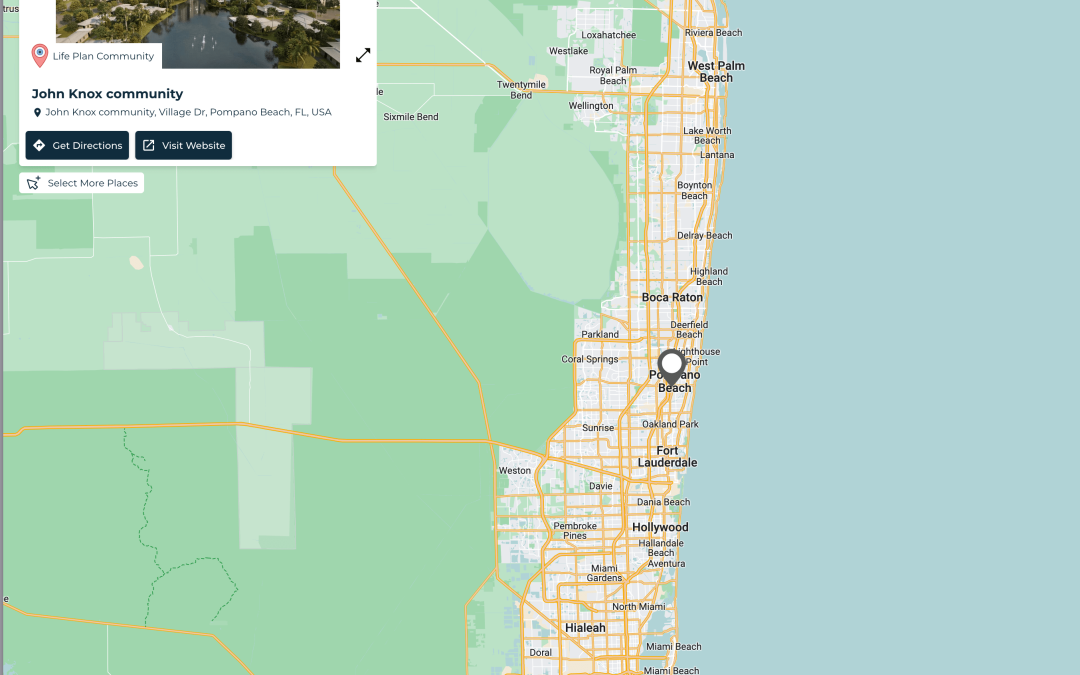

John Knox Village in Pompano Beach is a Premiere Life Plan Community in Florida.

At Second Act Financial Services, we specialize in helping seniors fund their Entry Fees through convenient bridge financing which we discuss more in detail below. Working with thousands of retirement communities across the USA our clients often tell us which communities they love.

John Knox Village in Pompano Beach is one such community! Seniors from all across the USA make the move to John Knox Village because it is a life and retirement destination!

As seniors prepare to make the move one question we hear all the time is “But how do I fund my Entry Fee?” We answer this question in today’s blog.

But First, Here are Nine Reasons Seniors Move to John Knox Village:

John Knox Village is located in the heart of Pompano Beach, Florida. It is a retirement community with one of the best reputations in the state of Florida as well as nationwide. With its cordial hospitality, variety of amenities, meaningful and vibrant lifestyle along with its highly regarded focus on quality care, John Knox Village presents an exciting way of life you simply cannot resist!

Here’s why seniors love John Knox Village:

1. Prime Coastal Location

John Knox Village is situated only minutes from the Atlantic Ocean, providing easy access for residents to some of the most beautiful beaches Florida has to offer. The warm climate and gentle ocean breezes make outdoor activities a true delight any time of the year. From days spent at the beach, walks along scenic shores, to simply basking in the sun-the coastal setting really enhances the quality of life for those residing here.

2. Vibrant and Inclusive Community

But perhaps the most impressive feature of John Knox Village is that of an active and truly inclusive community. It’s a very warm, family-like atmosphere in which the residents and staff alike go out of their way to make everyone feel welcome. Newcomers are welcomed right away; camaraderie is among the best, fostering an easy environment for making new, lasting friends. The active social scene provided throughout the year, from events to clubs and activities, endeavors to appeal to a wide range of interests within this diverse community.

The grounds at John Knox Village are immaculately kept and really prove to be quite the highlight. Lush landscaping, walking paths, and tranquil gardens make for a serene environment – one that is truly nature at its best. The community has focused on creating a peaceful, picturesque environment that adds to the quality of life encouraging its residents to spend much of their time engaged outdoors.

3. Wellness Programs

Wellness is top of mind daily at John Knox Village. You have a wide range of programs that support physical, mental, and emotional wellness. The state-of-the-art equipment and fitness classes offered in the Village Towers Fitness Studio are designed especially for senior adults, including yoga, Pilates, and aqua aerobics. In the interest of rounding out holistic health for the community, additional wellness coaching, nutrition workshops, and mental health services are provided daily. There is truly something for everyone at John Knox Village to strengthen both the body and mind.

4. Healthcare Services

Perhaps the biggest advantage of John Knox Village is the complete healthcare services available within the community for a sense of security among the residents as you age if needed. The care includes independent living, assisted living, memory care, and skilled nursing. For each service, personalized care plans are considered and developed to ensure each resident’s needs are met with care and empathy.

A variety of Life Care Contract options are offered by John Knox Village. You are encouraged to contact their sales office (a link to which is provided in the map below) for details on pricing and what contract options provide for a return of your Entry Fee either in whole or in part.

6. Cultural and Recreational Opportunities

The list of things to do at John Knox Village ranges from cultural trips to recreational activities, and is impressive to say the least. The Performing Arts Center gives way to concerts, theater productions, and lectures-all adding up to a very rich cultural life for the residents. In addition, the Village has a good arts program that involves things such as painting, pottery, and other creative activities. For those who enjoy staying active, there are also opportunities for swimming, golfing, and gardening.

7. Dining Excellence

Dining at John Knox Village transcends the simple act of enjoying a meal: it is an experience. With multiple dining venues to satisfy a wide variety of tastes, residents enjoy a unique ambiance married equally well to a pleasing menu selection. Savor gourmet meals prepared by talented chefs who can cater to everything from vegan to gluten-free and some in between. The emphasis on fresh, locally-sourced ingredients ensures that every meal will be healthy and tasty.

8. Emphasis on Lifelong Learning

Lifelong learning is a hallmark of the John Knox Village lifestyle. The community offers numerous educational programs, which range from current event lectures to technology, history, and the arts classes. These programs serve not only to keep the minds of the residents sharp but also to nurture a sense of curiosity and a love of learning that is very rewarding to many seniors.

9. Spiritual Enrichment

Throughout John Knox Village, spiritual fulfillment is attainable through numerous religious services and spiritual programs that are offered. Regular worship services, in-depth Bible study, and meditation are conducted within the community’s interfaith chapel. The community is very inclusive, and all the expressions of faith by residents are supported.

John Knox Village of Pompano Beach, Florida is unique. It is truly a retirement community that parallels the best in the nation. With its ideal coastal location, active community life, all-inclusive healthcare options, and wellness coupled with truly meaningful lifelong learning activities, it’s little wonder that so many seniors just love calling John Knox Village their home.

Now that you have learned why seniors love John Knox Village in Pompano Beach, how exactly do you fund your Entry Fee to this wonderful community?

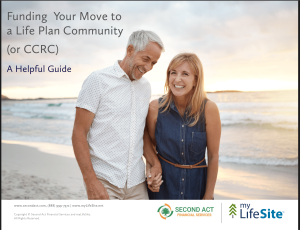

Download our free Guide here to learn about contract types offered by CCRCs and how seniors pay for their Entry Fee at John Knox Village in Pompano Beach and similar communities. Be sure to share this Guide with your family or professional financial advisors because they too will find it helpful!

Six Ways Seniors Fund their Entry Fees at John Knox Village in Pompano Beach Florida and other similar retirement communities.

1. Sale of Your Home:

Many seniors use the proceeds from the sale of their home as their “Entry” to John Knox Village. This strategy is very common, if not the most common way, seniors fund their Entry Fee to John Knox Village and other similar communities across the nation. But preparing the home for sale takes time.

Second Act Financial Services can connect you with the right real estate professionals who understand senior move management and can help coordinate the details for you at no charge. Whether you utilize the free assistance that can be provided by Second Act Financial Services or your own local realtor, be sure to follow these key points:

Always use experienced and reputable real estate agents. Not agents that are very part time. Sometimes your friend may not be the best agent. Make lists of what you want to keep, donate, and let go. Does the home need any repairs? It is important to work with a local agent who will help you find the handymen you need.

At Second Act we work to find agents willing to go the extra mile who will:

− Take professional photographs

− Help you de-clutter

− Properly stage and list your home

− Help you with your packing and moving

− Ensure you are comfortably moved into your new home

Enjoy life in your new community, while the Second Act Financial Services professionals work on your behalf and report to you every step of the way!

Call 888.999.7372 for immediate and prioritized assistance in selling your home!

2. Bridge Financing:

Most seniors usually sell their home and use the cash proceeds from their home sale to pay for their Entry Fee. For those seniors who would like to move into a CCRC first and enjoy the benefit of time to prepare, list and sell their home, a Home Equity Line of Credit for Senior Living such as the one offered by Second Act can act as a bridge loan for your CCRC entry fee. It is easier to clean, prepare, stage, list, and sell your home for the best price if you are not living in it.

How Second Act Bridge Loan Financing for Works:

– Apply for an overall line of credit amount.

– Draw what you need to fund your community’s Entrance Fee and monthly service fees.

– Make much smaller, interest-only payments on your outstanding balance.

– Enables you to enjoy the benefit of time so you can prepare and sell your home for the highest and best price.

– Pay back your line of credit when you have sold your home.

Seniors find it helpful to know that bridge financing is an often-used financial tool to help you move now while giving you the benefit of time to sell your home for the highest and best possible price.

Call 888.999.7372 to see if bridge financing by Second Act could be of help to you and to receive special, prioritized service.

3. Withdraws from Your Retirement Accounts:

There are many different types of retirement accounts, such as traditional IRAs, Roth IRAs, 401ks, and more. You may own more than one type of retirement account. When considering a withdrawal from a retirement account we strongly recommend a review of your options with a tax accountant and financial advisor before making any decisions. Large withdrawals from most IRAs (with the exception of Roth) will typically trigger a large income tax bill — potentially at a higher tax rate, and may also trigger a Medicare surcharge. A few hours of time with a tax professional could save you a lot of money in unexpected tax consequences.

First Step: Take Inventory of Your Accounts

The tax impact and potential withdrawal penalties vary by the type of retirement account. The first step in determining your options for potential withdrawals is to understand which types of accounts you have.

Be sure to visit www.secondact.com/LifePlan to learn about all the various types of retirement accounts, along with the most recent limits and details. While the page is not tax or financial advice, it can give you a good baseline for a conversation with professionals who specialize in tax and retirement account management.

4. “Margin Loans” – A Loan based on the value of your securities

If you have a sizeable investment account with a large brokerage firm, you may be able to obtain cash quickly by borrowing against their value. How much you can borrow depends on the firm. In some cases, you may be able to borrow up to 70% or more of the value of the underlying securities you post as collateral, depending on the size of the account. Sometimes referred to as a “portfolio loan” or a “securities-backed line-of-credit,” many investment and brokerage houses offer this kind of loan.

How does an investment loan work?

You select the securities you would like to borrow against, although there are restrictions. You then decide what percentage to borrow against, up to the maximum percentage allowed. The brokerage firm provides you with a Line of Credit that you can draw upon up to the approved credit limit. Funds are typically made available for use within days.

What are the pros and cons?

In a volatile market, large securities-backed loans can be somewhat risky because if the value of your account declines, you may have to post more collateral to keep the borrowing ratio in your loan agreement. Many seniors do not want the unpredictability that comes with a securities loan and opt for a Home Equity Line of Credit in its place. However, if the loan amount is relatively small compared to the overall account value, then the risk may be lower.

Many people do not realize that they can possibly take out a loan with their securities (investments such as stocks and mutual funds) serving as collateral. The amount you can borrow varies and depends on the parameters set by the investment or brokerage firm.

Typically, the securities loaned against cannot be sold or traded until the loan is paid back. And if the value of the securities declines past a certain amount you may have to post more collateral.

5. Sale of Your Securities:

Selling securities is also an often utilized approach to funding your Entry Fee. But be mindful because large and unintended tax consequences are not only triggered by withdrawals from retirement accounts, but potentially from other investments you hold, such as stocks, mutual funds, and ETFs which you decide you want to sell.

The amount of time you’ve held the shares, which shares you choose to sell, whether there is a gain or loss, and timing of the sale can all make a big difference in the potential tax due.

As of September 2024 the short-term capital gains tax is your ordinary income tax rate which ranges from 0% to 37%. And the long-term capital gains tax rate ranges between 0% – 20% again depending on your Adjusted Gross Income for the year.

6. Sale or Borrow from Your Life Insurance:

Life insurance is often purchased during the income-earning years so if the unexpected happens the survivors have adequate cash on hand to replace lost income and cover debt burdens. But as circumstances evolve, you may no longer have as much of a need for coverage.

If you find this to be the case, then your life insurance policy may be an asset you can tap into or even sell for cash. The possible options include:

Life Settlement

The most common life settlement solution is an all-cash lump-sum payment to the policy owner where the purchaser takes over all future premium obligations and becomes the beneficiary

Exchange to an Annuity

You may be able to do a tax-free 1035 exchange of your life insurance policy into an annuity, which can then be used to provide a guaranteed income stream for a period or for life. This may not necessarily help pay the entry fee directly, but it may help replace income that otherwise would have come from other assets you choose to sell.

Long-Term Care Benefit

Many life insurance policies include a rider for long-term care insurance. Yet, there are other types of hybrid policies available that still provide life insurance but also include substantially more coverage for long-term care. You may have the option to convert your life insurance policy to a hybrid policy if it makes sense for your unique situation and financial plans.

Retained Benefit

You may also decide to keep a portion of your coverage intact with no future premium obligations.

If you have a life insurance policy in the amount of $100,000 or greater and want to explore your options, call the Second Act Financial Services number below for prioritized service.

Call 888.999.7372 to be connected to a life insurance sale options for your consideration with prioritized care and service.

Important Disclaimer

The information in this page is not meant to serve as financial, tax, or personal financial planning advice. No decisions should be made from reading the information on this page. Decisions should be made after careful analysis and consultation with your financial, tax, accounting, or other professional advisor licensed to provide retirement advice. Second Act is a Division of Liberty Savings Bank, F.S.B. Member FDIC. Lending and loan services provided by Liberty Savings Bank, F.S.B. NMLS # 408905. Equal Housing Lender. All other services provided by Second Act Financial Services, LLC. This information is current as of 1/01/2024. Subject to credit and loan approval. Conditions and limitations apply. Information, rates and terms are subject to change without notice. © 2024 Second Act Financial Services, LLC. All Rights Reserved.

Recent Comments