How seniors pay for their CCRC Entry Fee is as important a question as which CCRC is right for you. Many seniors who move to a life plan community choose to sell a primary residence and use the proceeds to cover most or all of their entry fee. For others who no longer own a home this may not be an option. And still for other seniors, the move to a life plan community may require the combination of selling a home and withdrawing from assets.

But there are also other potential options available to help you fund the move to a life plan community, including senior living bridge loans such as those provided by Second Act, short term loans against securities, and tapping into cash available from life insurance policies that may no longer be needed.

How do Seniors Pay for their CCRC Entry Fee? The Six Ways Seniors Typically Utilize to Fund their Entry Fee in a CCRC or Life Plan Community are:

1. Retirement Account Withdrawals

2. Selling Your Home

3. Bridge Loans in the form of a Home Equity Line of Credit such as those provided by Second Act

4. Sales of Securities

5. Loan Against Securities

6. Sale, Exchange, or Borrow from Life Insurance

1. Retirement Account Withdrawals

There are many different types of retirement accounts, such as traditional IRAs, Roth IRAs, 401ks, and more. You may own more than one type of retirement account. When considering a withdrawal from a retirement account we strongly recommend a review of your options with a tax accountant and financial advisor before making any decisions. Large withdrawals from most IRAs (with the exception of Roth) will typically trigger a large income tax bill — potentially at a higher tax rate, and may also trigger a Medicare surcharge. A few hours of time with a tax professional could save you a lot of money in unexpected tax consequences.

First Step: Take Inventory of Your Accounts

The tax impact and potential withdrawal penalties vary by the type of retirement account. The first step in determining your options for potential withdrawals is to understand which types of accounts you have.

Be sure to visit www.secondact.com/LifePlan to learn about all the various types of retirement accounts, along with the most recent limits and details. While the page is not tax or financial advice, it can give you a good baseline for a conversation with professionals who specialize in tax and retirement account management.

It is important before you withdraw from any retirement accounts to get professional guidance . The most important step when it comes to potential withdrawals from an account is to make sure you consult a tax professional first. Before you visit with your tax and financial advisors, review the account withdrawal tax considerations for your retirement account types at www.secondact.com/LifePlan.

2. Selling Your Home for the Best Price

Your home is one of your most valuable and most treasured assets. If you plan to sell your home to help cover the cost of an entrance fee at a life plan community, you may be able to obtain a higher price for your home with a little preparation.

Second Act Financial Services can connect you with the right real estate professionals who understand senior move management and can help coordinate the details for you at no charge. Whether you utilize the free assistance that can be provided by Second Act Financial Services or your own local realtor, be sure to follow these key points:

Always use experienced and reputable real estate agents. Not agents that are very part time. Sometimes your friend may not be the best agent.

Make lists of what you want to keep, donate, and let go.

Does the home need any repairs? Working with the local agent we can find the right help to get your home ready to sell.

Find agents willing to go the extra mile who will:

− Take professional photographs

− Help you de-clutter

− Properly stage and list your home

− Help you with your packing and moving

− Ensure you are comfortably moved into your new home

Enjoy life in your new community, while the Second Act Financial Services professionals work on your behalf and report to you every step of the way! Call 888.999.7372 for immediate and prioritized assistance in selling your home.

3. Bridge Loans: Home Equity Line of Credit for Senior Living

There are times when you are ready to make the move to a retirement community quickly. Maybe it’s to lock in a community promotion or before a change in health. Maybe it’s because you think your home value is at a peak and you don’t want to wait any longer to list it. Whatever the case, a home equity line of credit for senior living can act as a bridge loan.

Second Act, a senior-focused division of Liberty Savings Bank, F.S.B. of Wilmington OH, specializes in offering this type of line, with a fast process that is tailor-made for senior living consumers. Even if your home is listed, you can still obtain this Home Equity Line of Credit for Senior Living, something many banks won’t do.

Bridge loans specially tailored for the retirement community or senior living move provide financial flexibility and give you time to prepare and sell your home for the highest and best price. Thousands of seniors take advantage of bridge financing to move sooner.

It’s easier to clean, prepare, list and show a home when you are not living in it. The cost of the bridge loan often seems small compared to the financial benefits of a higher home sale price.

How Second Act Bridge Loan Financing for Works:

– Apply for an overall line of credit amount.

– Draw what you need to fund your community’s Entrance Fee and monthly service fees.

– Make much smaller, interest-only payments on your outstanding balance.

– Enables you to enjoy the benefit of time so you can prepare and sell your home for the highest and best price.

– Pay back your line of credit when you have sold your home.

Whether you work with Second Act, your local bank, or a Credit Union, it’s helpful to know that bridge financing is an often-used financial tool to help you move now while giving you the benefit of time to sell your home for the highest and best possible price.

Call 888.999.7372 to see if bridge financing by Second Act could be of help to you and to receive special, prioritized service.

4. Sale of Securities

Large and unintended tax consequences are not only triggered by withdrawals from retirement accounts, but potentially from other investments you hold, such as stocks, mutual funds, and ETFs. The amount of time you’ve held the shares, which shares you choose to sell, whether there is a gain or loss, and timing of the sale can all make a big difference in the potential tax due.

For example, if you sell a stock or ETF that you’ve held for longer than one year it is likely you’ll pay capital gains tax on the difference between your investment (cost basis) and the value at the time of sale. If you’ve held the security for less than a year, you will pay the short-term capital gains tax, which is equivalent to your income tax rate in the year of sale. This rate could be higher than the long-term capital gains rate, particularly if you still have earned income. However, even the amount of long-term capital gains tax you will pay is based on your adjusted gross income. The long-term capital gains tax ranges from 0% to 20%, depending on your adjusted gross income for the year. Keep in mind that state taxes may also be due.

Consider this scenario for a moment. Suppose you decide to take a withdrawal from your IRA and at the same time liquidate other securities held outside of an IRA. The withdrawal from the IRA could put you in a higher ordinary income tax bracket, which could also potentially cause you to pay a higher capital gains tax rate on the sale of your non-IRA securities.

In some cases, it could make sense to offset capital gains on the sale of an investment by selling another investment at a loss because you can typically use capital losses to offset capital gains. As of May 2023, short term capital gains are taxed at ordinary income tax rates ranging from 0–37%.

Long-term capital gains federal taxes are between 0–20%, depending on your AGI. Selling securities to fund your entry fee or purchase in a life plan community could make sense for you if necessary, but be sure to discuss it with a tax professional and/or financial advisor before making any decisions.

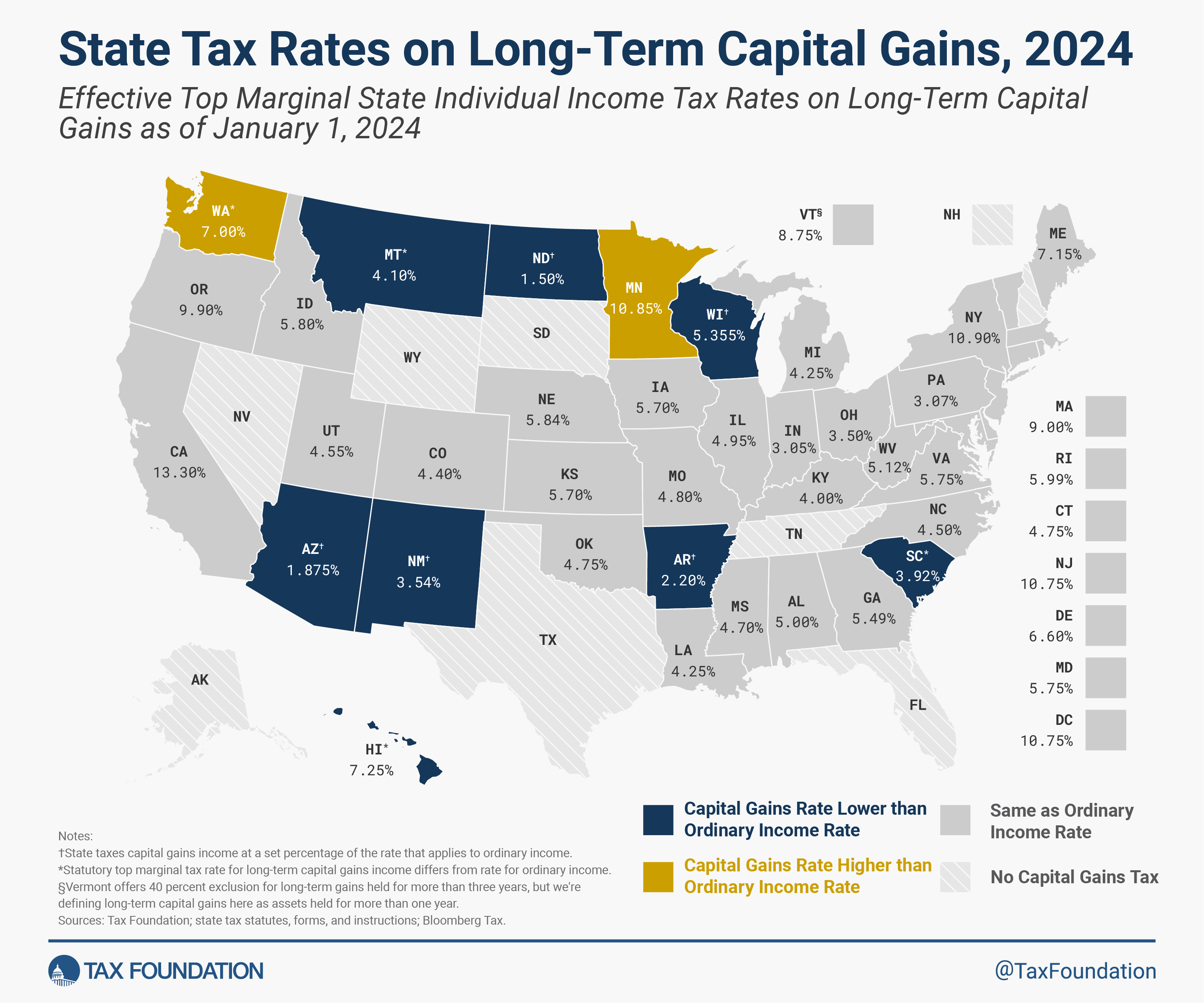

It is also important to bear in mind that in addition to federal capital gains taxes you may have state capital gains taxes as well.According to the TaxFoundation.org the state tax burden for long-term capital gains as of 2024 is as follows:

5. Loan Against Your Securities (frequently called Margin Loans)

If you have a sizeable investment account with a large brokerage firm, you may be able to obtain cash quickly by borrowing against their value. How much you can borrow depends on the firm. In some cases, you may be able to borrow up to 70% or more of the value of the underlying securities you post as collateral, depending on the size of the account. Sometimes referred to as a “portfolio loan” or a “securities-backed line-of-credit,” many investment and brokerage houses offer this kind of loan.

How does an investment loan work?

You select the securities you would like to borrow against, although there are restrictions. You then decide what percentage to borrow against, up to the maximum percentage allowed. The brokerage firm provides you with a Line of Credit that you can draw upon up to the approved credit limit. Funds are typically made available for use within days.

What are the pros and cons?

In a volatile market, large securities-backed loans can be somewhat risky because if the value of your account declines, you may have to post more collateral to keep the borrowing ratio in your loan agreement. Many seniors do not want the unpredictability that comes with a securities loan and opt for a Home Equity Line of Credit in its place. However, if the loan amount is relatively small compared to the overall account value, then the risk may be lower.

Many people do not realize that they can possibly take out a loan with their securities (investments such as stocks and mutual funds) serving as collateral. The amount you can borrow varies and depends on the parameters set by the investment or brokerage firm.

Typically, the securities loaned against cannot be sold or traded until the loan is paid back. And if the value of the securities declines past a certain amount you may have to post more collateral.

6. Selling or Borrowing from your Life Insurance Policy

Many people do not think of their life insurance policy as a financial asset. But did you know that you have the option to sell it if you no longer need the coverage? You may also have the option to convert it to an annuity or a hybrid policy with long-term care insurance included? If your policy has a substantial build-up of cash value, you may also be able to access the cash in a tax efficient manner.

Life insurance is often purchased during the income-earning years so if the unexpected happens the survivors have adequate cash on hand to replace lost income and cover debt burdens. But as circumstances evolve, you may no longer have as much of a need for coverage.

If you find this to be the case, then your life insurance policy may be an asset you can tap into or even sell for cash. The possible options include:

Life Settlement

The most common life settlement solution is an all-cash lump-sum payment to the policy owner where the purchaser takes over all future premium obligations and becomes the beneficiary

Exchange to an Annuity

You may be able to do a tax-free 1035 exchange of your life insurance policy into an annuity, which can then be used to provide a guaranteed income stream for a period or for life. This may not necessarily help pay the entry fee directly, but it may help replace income that otherwise would have come from other assets you choose to sell.

Long-Term Care Benefit

Many life insurance policies include a rider for long-term care insurance. Yet, there are other types of hybrid policies available that still provide life insurance but also include substantially more coverage for long-term care. You may have the option to convert your life insurance policy to a hybrid policy if it makes sense for your unique situation and financial plans.

Retained Benefit

You may also decide to keep a portion of your coverage intact with no future premium obligations.

If you have a life insurance policy in the amount of $100,000 or greater and want to explore your options, call the Second Act Financial Services number below for prioritized service.

Call 888.999.7372 to be connected to a life insurance sale options for your consideration with prioritized care and service.

A Summary of Questions to Consider Before Deciding How to Best Fund Your Entry Fee

If you are considering a move to a life plan community, the below questions are a summary of all that you read above. Take this article with you at your appointment with your financial and tax advisors. Moving to a Continuing Care Retirement Community (CCRC) or Life Plan Community can be a wonderful and great next step in your life. The peace of mind you gain with these communities’ life care contracts is priceless. Combine it with the active, vibrant, lifestyle, and you have the best of both worlds: a meaningful life with care for life:

• Does my home have enough equity to cover most or all of the entry fee?

• Will there be capital gains taxes due on the sale of my home?

• How quickly can I sell my home?

• What will I need to do to ensure I obtain the best price for my home?

• Could bridge financing in the form of a Home Equity Line of Credit for Senior Living help by allowing me to move now while having more time to sell my home?

• What other funds do I have that may be available to use towards the entrance fee?

• Is a short-term security backed loan a possibility for me to help cover the entry fee until my home sales?

• Do I have life insurance policies that are no longer needed for their originally intended purpose?

• What will be the tax and financial planning implications of taking a withdrawal from an investment account or a retirement account?

Before taking substantial withdrawals from an account or utilizing other financial options described in this guide, be sure to seek the guidance of a qualified and experienced tax and financial advisor who can help you determine not only the potential tax due on the transaction, but also how it may affect your overall tax rate. You will need to consider not only federal taxes but your state’s income or capital gains taxes. Many states tax capital gains in addition to the tax levied by the federal government.

About Second Act Financial Services

At Second Act Financial Services, we specialize in navigating CCRC financing challenges. Our team brings extensive experience in retirement and banking solutions, focusing on home sale solutions, home equity lines of credit that can serve as bridge loan solutions, and connections to veteran benefits, long-term care insurance or life settlement resources. We help you understand your options for managing CCRC entry fees and provide support with our financial options every step of the way. Our proven track record in assisting clients with their retirement financing needs reflects our commitment to your financial well-being. Trust us to guide you with expertise as you plan for life in your chosen retirement community. For more information on how we can assist you, visit Second Act Financial Services.

Important Disclaimer

The information in this page is not meant to serve as financial, tax, or personal financial planning advice. No decisions should be made from reading the information on this page. Decisions should be made after careful analysis and consultation with your financial, tax, accounting, or other professional advisor licensed to provide retirement advice.

Second Act is a Division of Liberty Savings Bank, F.S.B. Member FDIC. Lending and loan services provided by Liberty Savings Bank, F.S.B. NMLS # 408905. Equal Housing Lender. All other services provided by Second Act Financial Services, LLC. This information is current as of 1/01/2024. Subject to credit and loan approval. Conditions and limitations apply. Information, rates and terms are subject to change without notice. © 2024 Second Act Financial Services, LLC. All Rights Reserved.

Recent Comments